Ten-Column Worksheets

The 10-column worksheet is an all-in-one spreadsheet showing the transition of account information from the unadjusted trial balance through the financial statements. Accountants use the 10-column worksheet to help calculate end-of-period adjustments. Using a 10-column worksheet is an optional step companies may use in their accounting process.

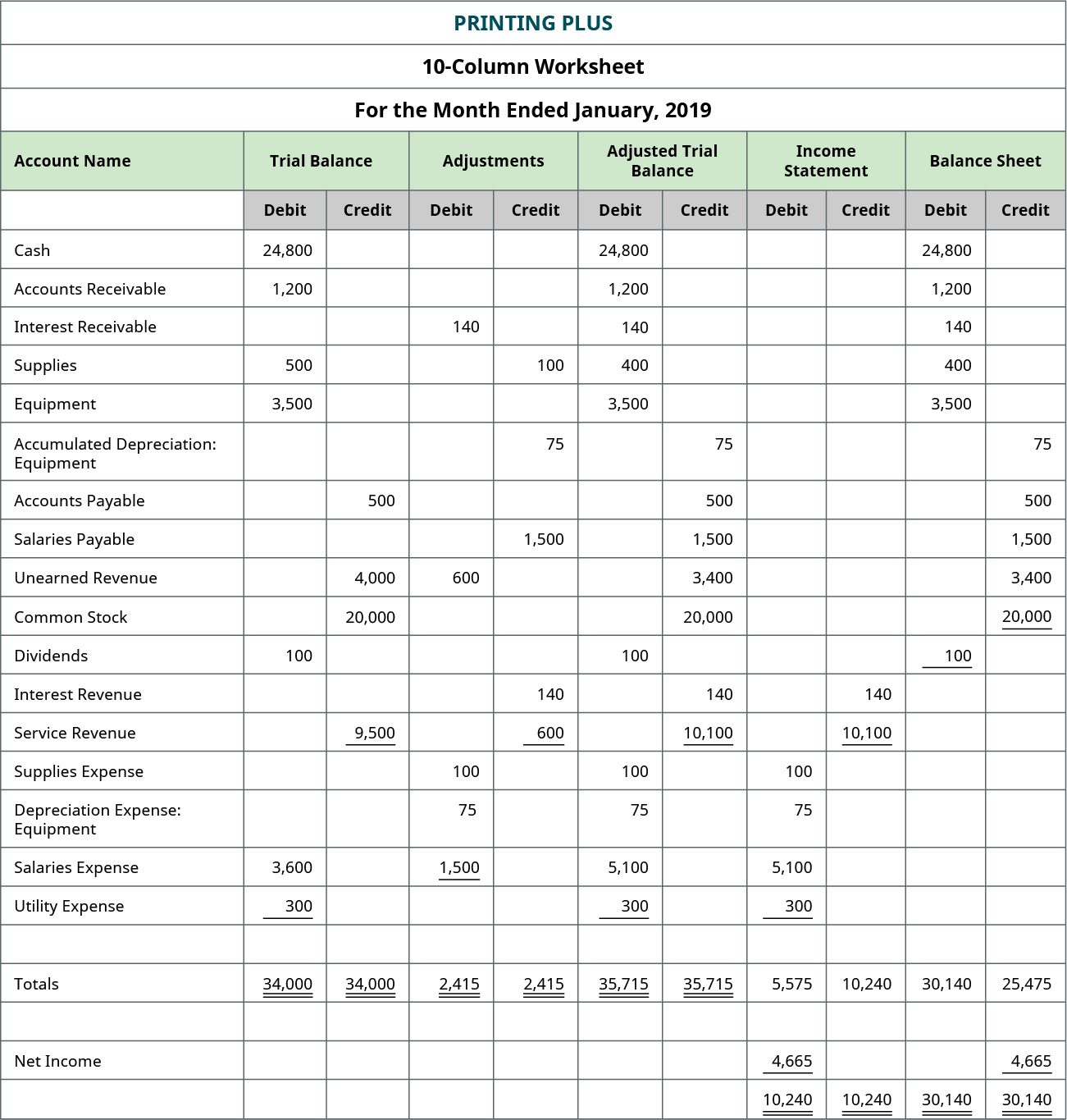

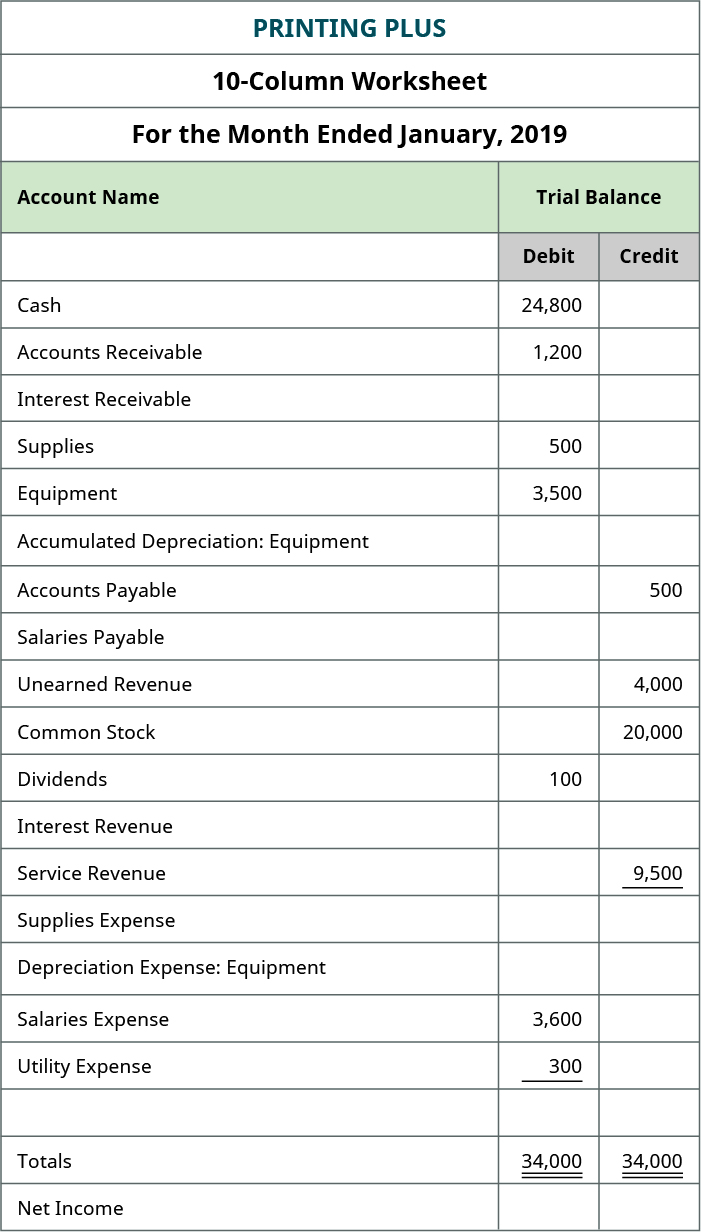

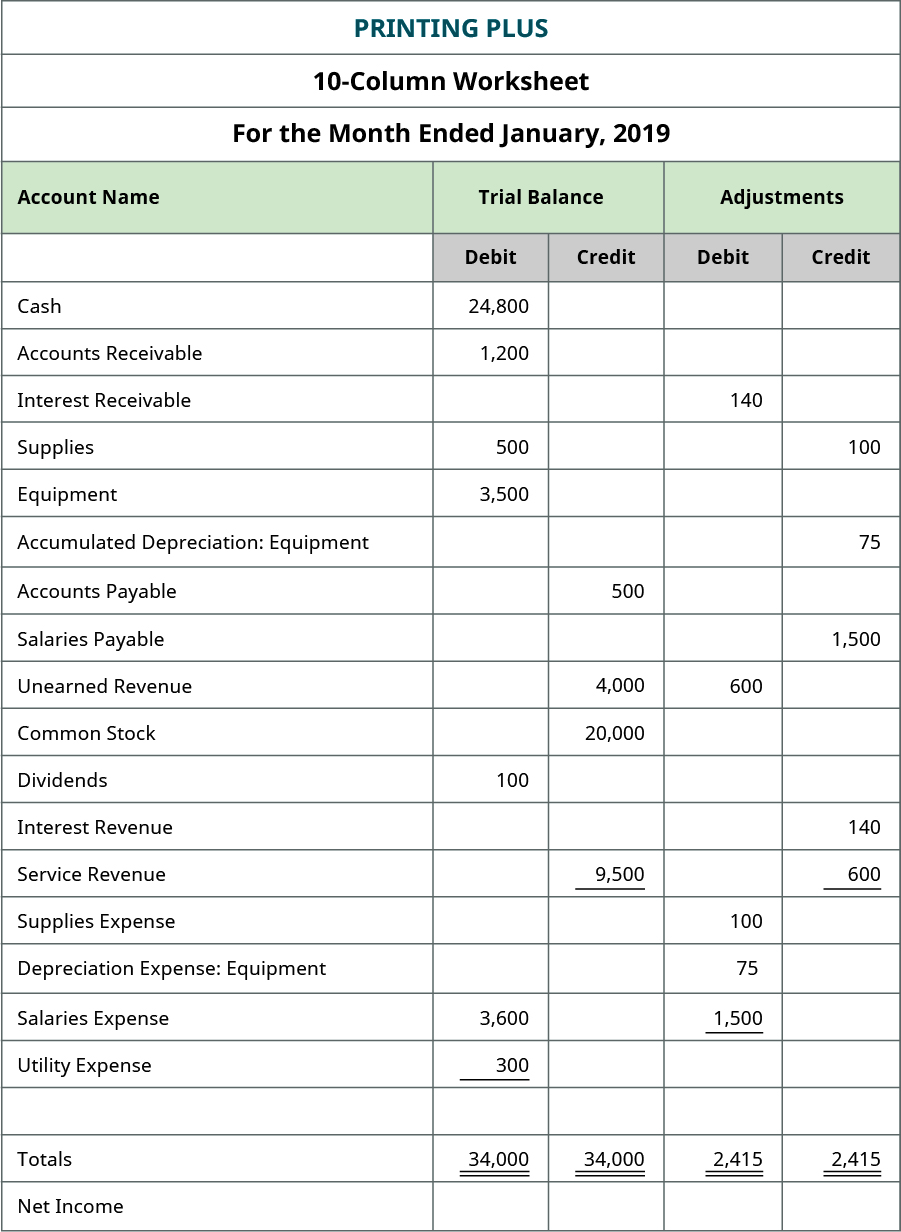

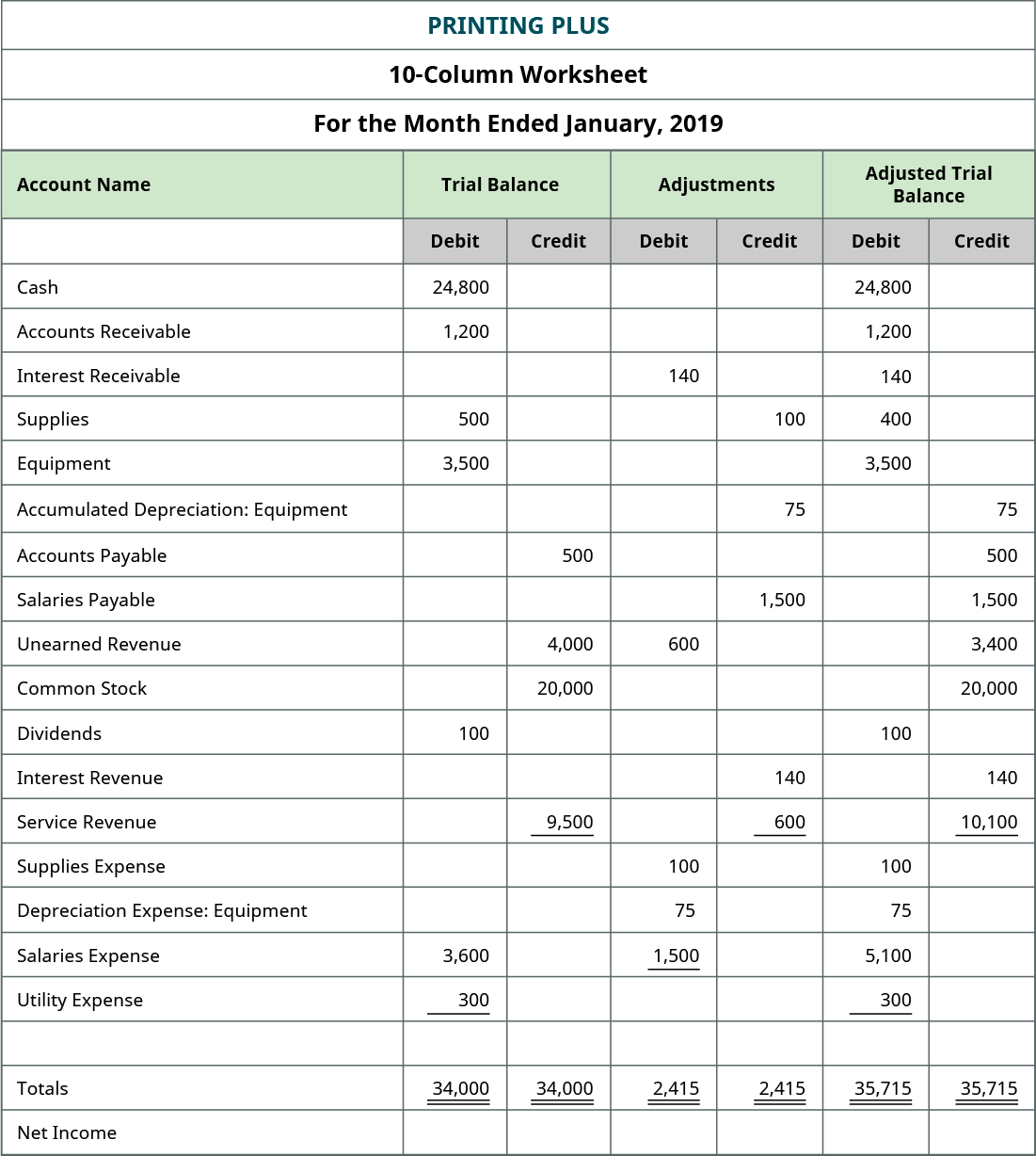

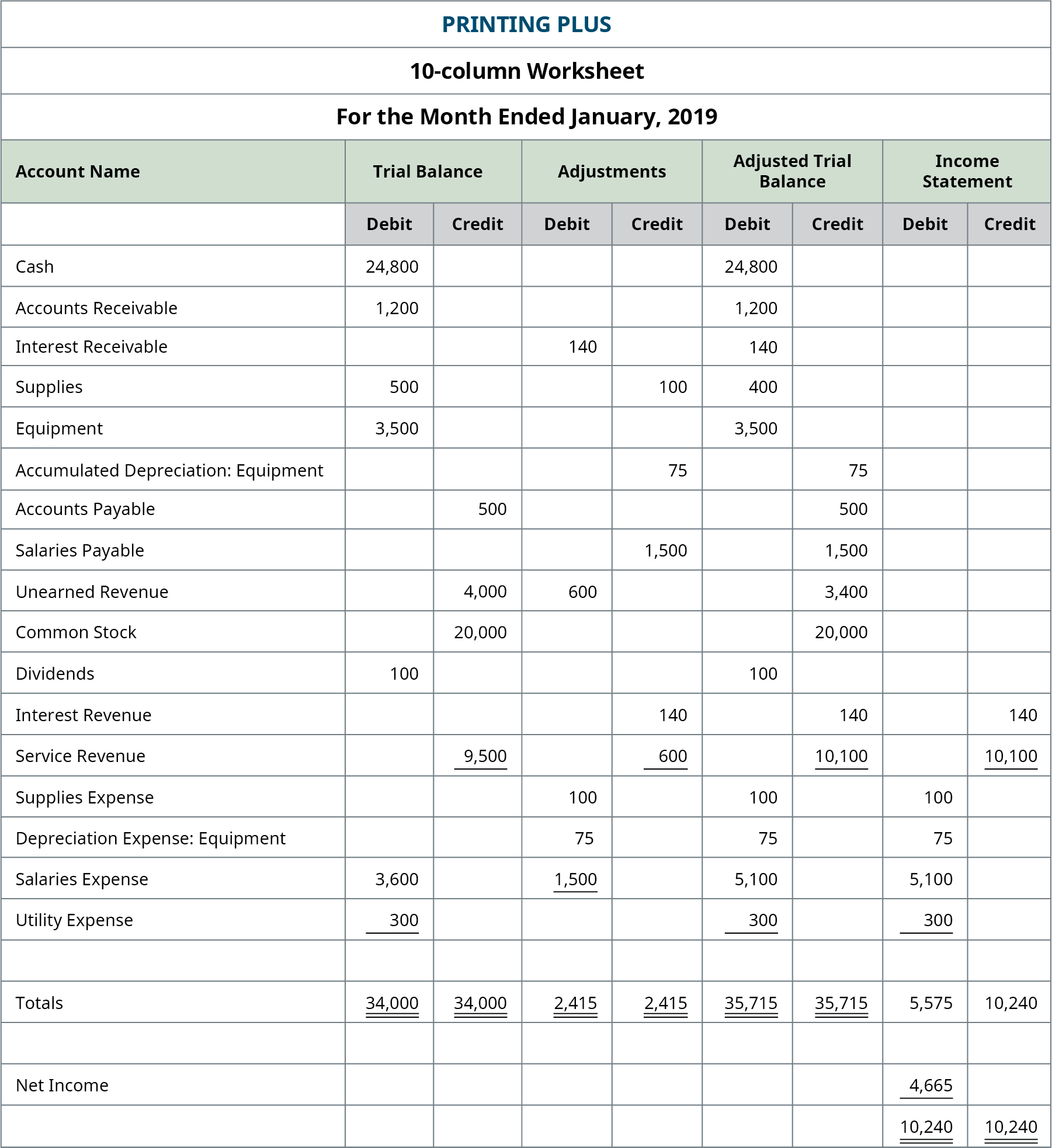

Here is a picture of a 10-column worksheet for Printing Plus.

There are five sets of columns, each set having a column for debit and credit, for a total of 10 columns. The five column sets are the trial balance, adjustments, adjusted trial balance, income statement, and the balance sheet. After a company posts its day-to-day journal entries, it can begin transferring that information to the trial balance columns of the 10-column worksheet.

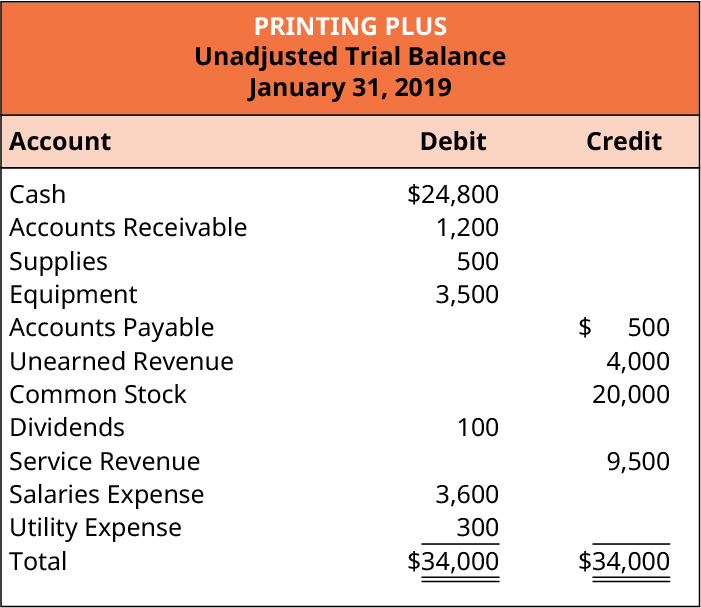

The trial balance information for Printing Plus is shown previously. Notice that the debit and credit columns both equal $34,000. If we go back and look at the trial balance for Printing Plus, we see that the trial balance shows debits and credits equal to $34,000.

Once the trial balance information is on the worksheet, the next step is to fill in the adjusting information from the posted adjusted journal entries.

The adjustments total of $2,415 balances in the debit and credit columns.

The next step is to record information in the adjusted trial balance columns.

To get the numbers in these columns, you take the number in the trial balance column and add or subtract any number found in the adjustment column. For example, Cash shows an unadjusted balance of $24,800. There is no adjustment in the adjustment columns, so the Cash balance from the unadjusted balance column is transferred over to the adjusted trial balance columns at $24,800. Interest Receivable did not exist in the trial balance information, so the balance in the adjustment column of $140 is transferred over to the adjusted trial balance column.

Unearned revenue had a credit balance of $4,000 in the trial balance column, and a debit adjustment of $600 in the adjustment column. Remember that adding debits and credits is like adding positive and negative numbers. This means the $600 debit is subtracted from the $4,000 credit to get a credit balance of $3,400 that is translated to the adjusted trial balance column.

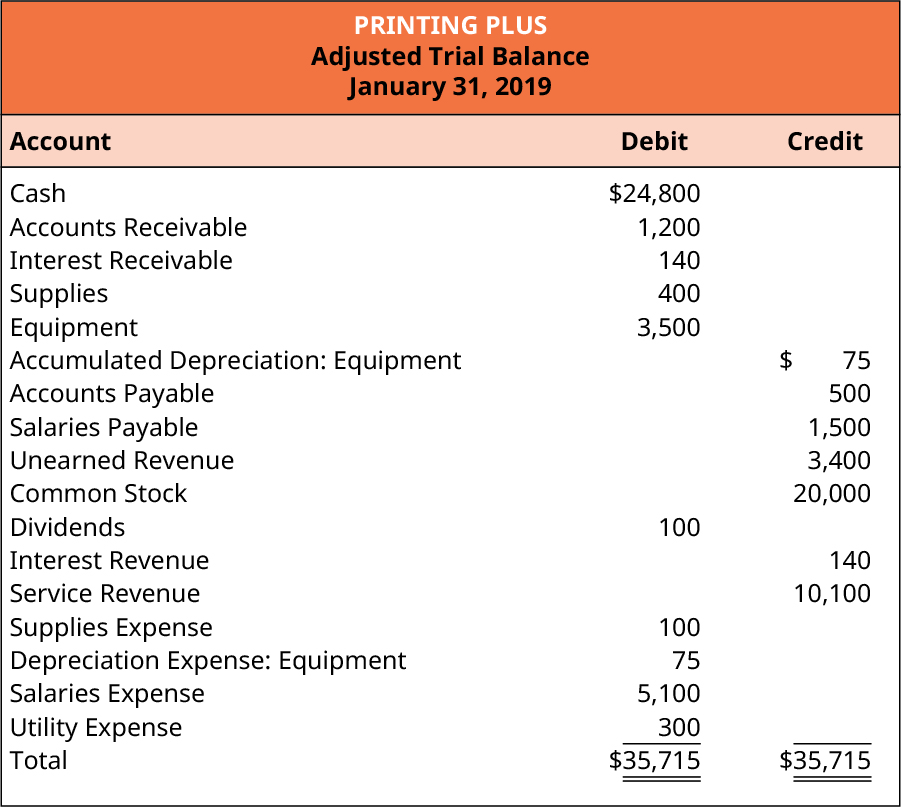

Service Revenue had a $9,500 credit balance in the trial balance column, and a $600 credit balance in the Adjustments column. To get the $10,100 credit balance in the adjusted trial balance column requires adding together both credits in the trial balance and adjustment columns (9,500 + 600). You will do the same process for all accounts. Once all accounts have balances in the adjusted trial balance columns, add the debits and credits to make sure they are equal. In the case of Printing Plus, the balances equal $35,715. If you check the adjusted trial balance for Printing Plus, you will see the same equal balance is present.

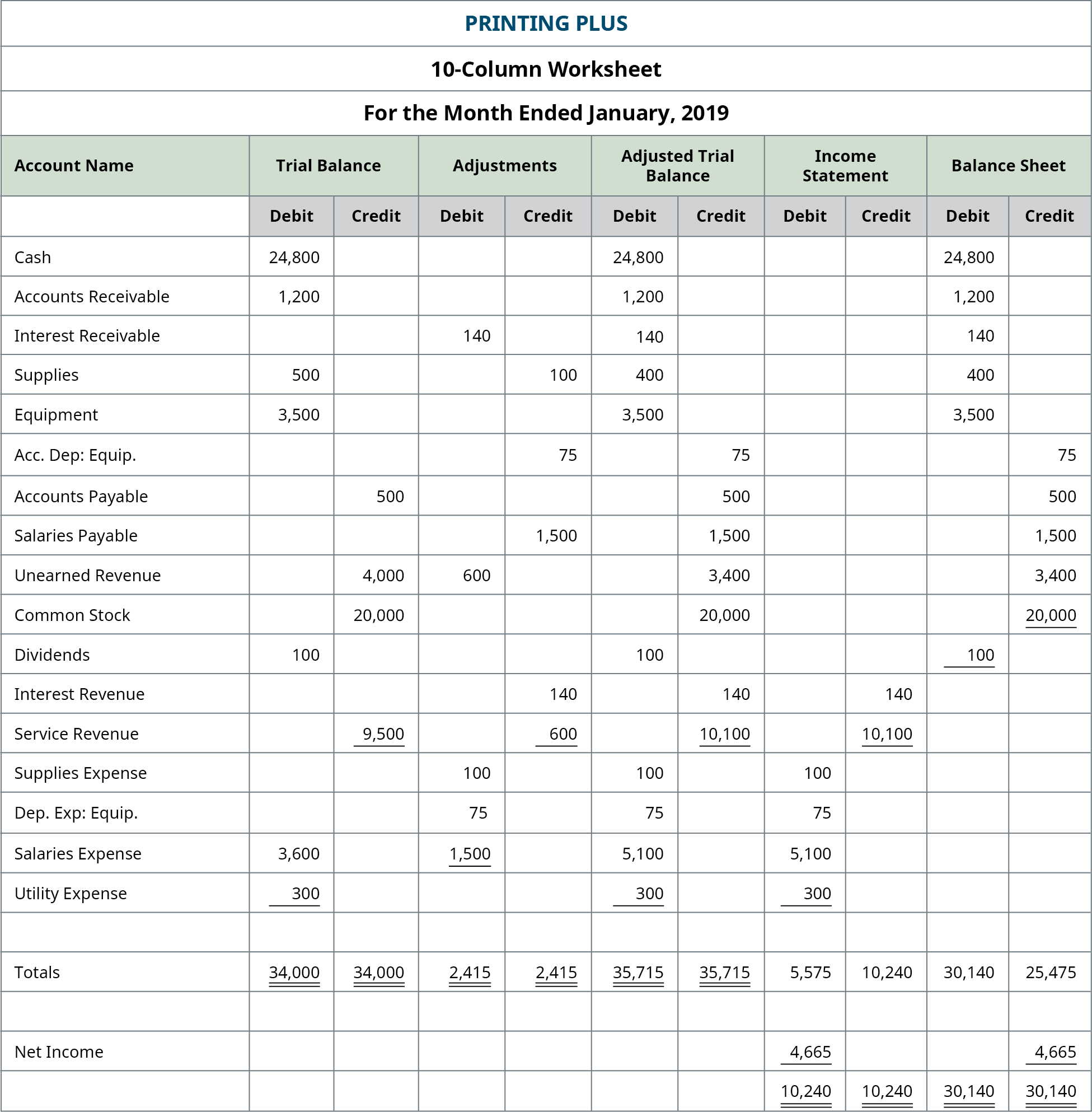

Next you will take all of the figures in the adjusted trial balance columns and carry them over to either the income statement columns or the balance sheet columns.

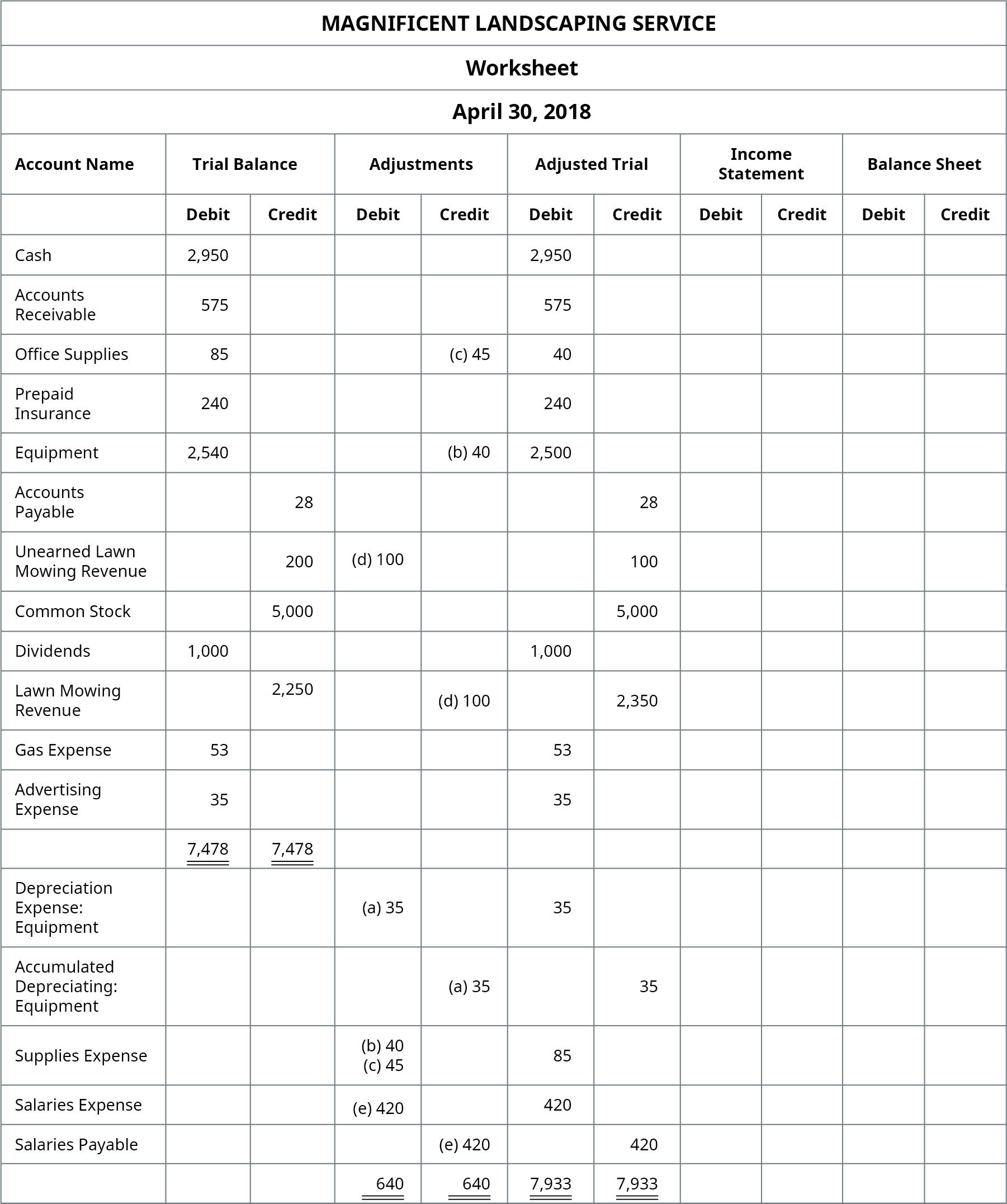

YOUR TURN

Take a couple of minutes and fill in the income statement and balance sheet columns. Total them when you are done. Do not panic when they do not balance. They will not balance at this time.

Solution

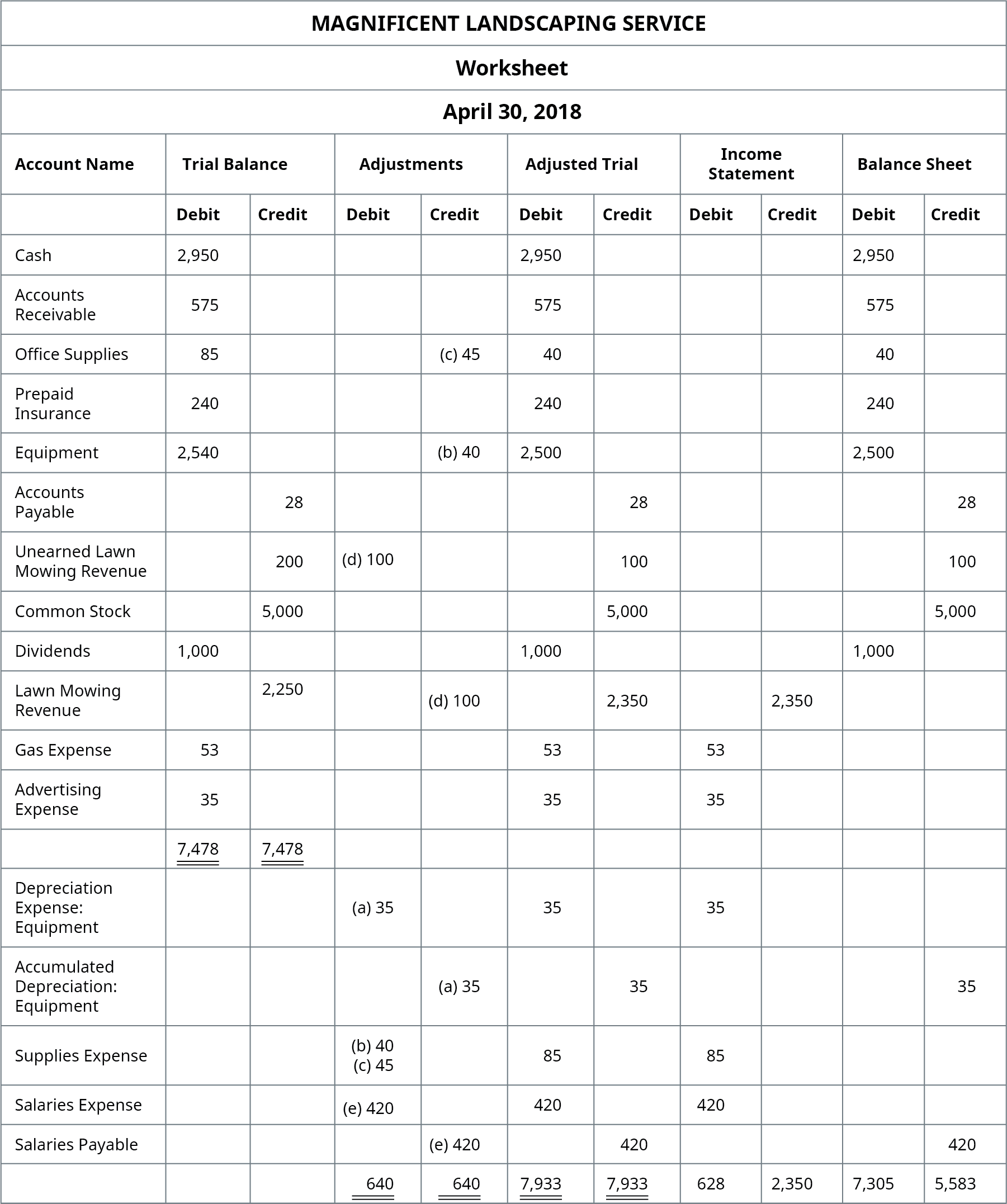

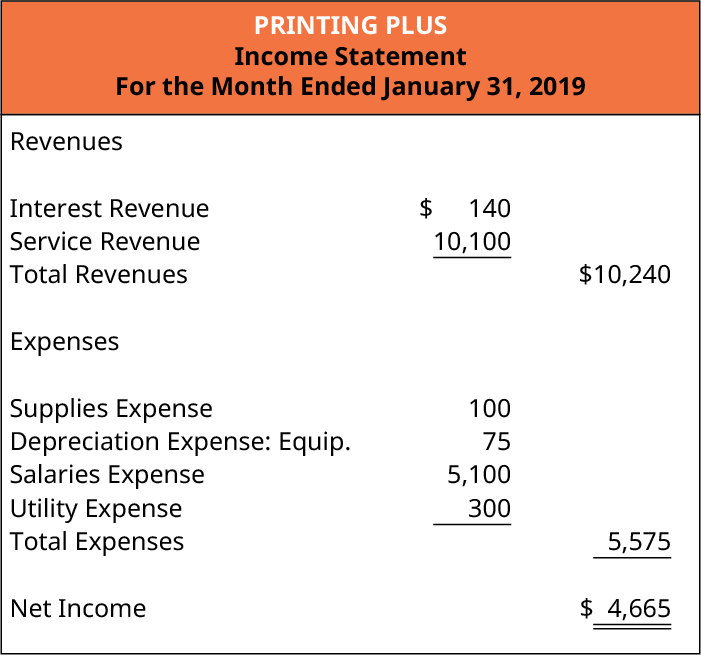

Looking at the income statement columns, we see that all revenue and expense accounts are listed in either the debit or credit column. This is a reminder that the income statement itself does not organize information into debits and credits, but we do use this presentation on a 10-column worksheet.

You will notice that when debit and credit income statement columns are totaled, the balances are not the same. The debit balance equals $5,575, and the credit balance equals $10,240. Why do they not balance?

If the debit and credit columns equal each other, it means the expenses equal the revenues. This would happen if a company broke even, meaning the company did not make or lose any money. If there is a difference between the two numbers, that difference is the amount of net income, or net loss, the company has earned.

In the Printing Plus case, the credit side is the higher figure at $10,240. The credit side represents revenues. This means revenues exceed expenses, thus giving the company a net income. If the debit column were larger, this would mean the expenses were larger than revenues, leading to a net loss. You want to calculate the net income and enter it onto the worksheet. The $4,665 net income is found by taking the credit of $10,240 and subtracting the debit of $5,575. When entering net income, it should be written in the column with the lower total. In this instance, that would be the debit side. You then add together the $5,575 and $4,665 to get a total of $10,240. This balances the two columns for the income statement. If you review the income statement, you see that net income is in fact $4,665.

We now consider the last two columns for the balance sheet. In these columns we record all asset, liability, and equity accounts.

When adding the total debits and credits, you notice they do not balance. The debit column equals $30,140, and the credit column equals $25,475. How do we get the columns to balance?

Treat the income statement and balance sheet columns like a double-entry accounting system, where if you have a debit on the income statement side, you must have a credit equaling the same amount on the credit side. In this case we added a debit of $4,665 to the income statement column. This means we must add a credit of $4,665 to the balance sheet column. Once we add the $4,665 to the credit side of the balance sheet column, the two columns equal $30,140.

You may notice that dividends are included in our 10-column worksheet balance sheet columns even though this account is not included on a balance sheet. So why is it included here? There is actually a very good reason we put dividends in the balance sheet columns.

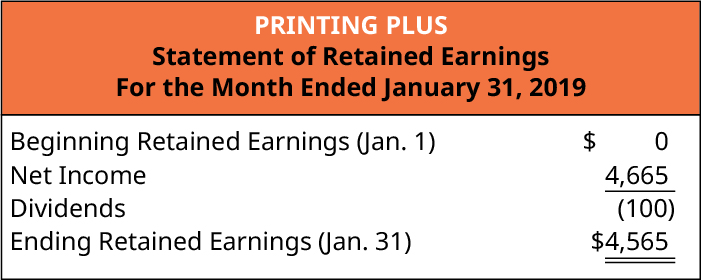

When you prepare a balance sheet, you must first have the most updated retained earnings balance. To get that balance, you take the beginning retained earnings balance + net income – dividends. If you look at the worksheet for Printing Plus, you will notice there is no retained earnings account. That is because they just started business this month and have no beginning retained earnings balance.

If you look in the balance sheet columns, we do have the new, up-to-date retained earnings, but it is spread out through two numbers. You have the dividends balance of $100 and net income of $4,665. If you combine these two individual numbers ($4,665 – $100), you will have your updated retained earnings balance of $4,565, as seen on the statement of retained earnings.

You will not see a similarity between the 10-column worksheet and the balance sheet, because the 10-column worksheet is categorizing all accounts by the type of balance they have, debit or credit. This leads to a final balance of $30,140.

The balance sheet is classifying the accounts by type of accounts, assets and contra assets, liabilities, and equity. This leads to a final balance of $29,965. Even though they are the same numbers in the accounts, the totals on the worksheet and the totals on the balance sheet will be different because of the different presentation methods.

LINK TO LEARNING

YOUR TURN

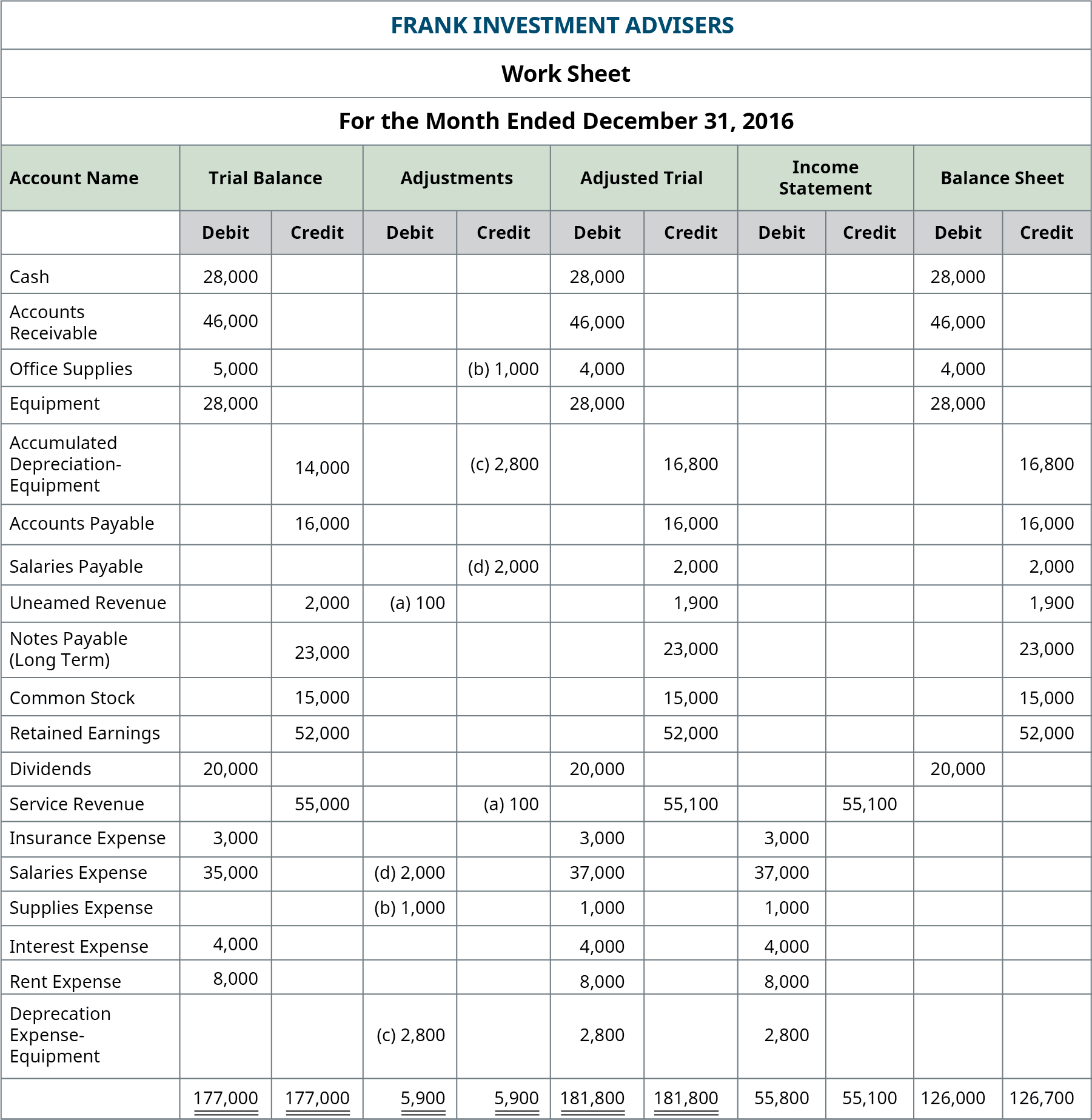

What amount of net income/loss does Frank have?

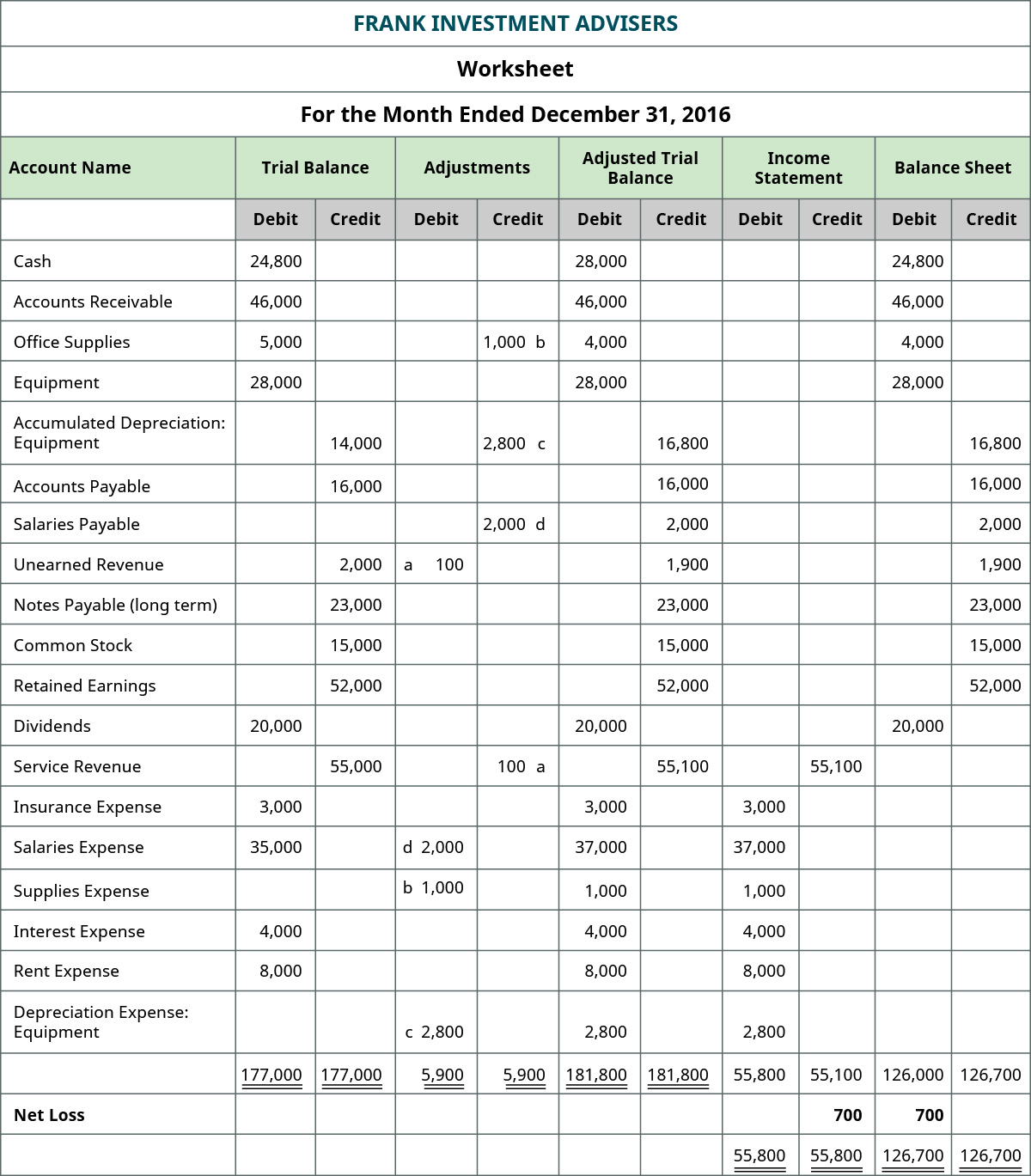

Solution

In Completing the Accounting Cycle, we continue our discussion of the accounting cycle, completing the last steps of journalizing and posting closing entries and preparing a post-closing trial balance.

KEY TAKEAWAYS

Key Concepts and Summary

- 10-column worksheet: The 10-column worksheet organizes data from the trial balance all the way through the financial statements.

an all-in-one spreadsheet showing the transition of account information from the trial balance through the financial statements